27 juillet 2023

Securities and Exchange Commission

Division of Corporation Finance

Office of Crypto Assets

100 F Street, NE

Washington, D.C. 20549

Attn: Kate Tillan and Rolf Sundwall

| Re: | Bitfarms LTD |

| Form 40-F for the Fiscal Year Ended December 31, 2022 | |

| Filed March 21, 2023 | |

| File No. 001-40370 |

Dear Ms. Tillan and Mr. Sundwall,

On behalf of Bitfarms Ltd (the “Company”), I am responding to the comments contained in the letter dated June 26, 2023 (the “Letter”) from the staff of the Securities and Exchange Commission (the “Commission” and, the staff of the Commission, the “Staff”) to Jeffrey Lucas, Chief Financial Officer of the Company, relating to the Company’s Form 40-F for the fiscal year ended December 31, 2022 (the “2022 40-F”). The responses contained herein are keyed to the numbers of the comments in the Letter, which appear in italics below for convenience of reference. Unless otherwise indicated, capitalized terms used herein have the meanings assigned to them in the 2022 40-F. As an initial matter, the Company notes that the only digital assets mined, purchased and sold by the Company during the years ended December 31, 2021 and 2022 as well as year to date in 2023 were Bitcoin.

In addition, as noted in further detail below, the following appendices are included with this response to the information requested in the Letter:

| ● | Appendix A – Mining pool service agreement |

| ● | Appendix B – Mining pool payout methodology |

| 1. | You classify proceeds from the sale of digital assets mined within cash related to operating activities. Please tell us how you considered IAS 7.16(b) which gives cash receipts from sales of intangible assets as an example of cash flows arising from investing activities. Provide us the general time frame you hold cryptocurrencies mined, including the average, maximum and minimum time you held them during the periods presented. |

Response: IAS 7.14 describes cash flows from operating activities as being primarily derived from the principal revenue-producing activities of the entity. Therefore, cash flows from operations generally result from the transactions and other events that enter into the determination of profit or loss.

In applying this principle for classification purposes, the Company classifies cash flows from the sale of Bitcoin based on the transaction or event that originally gave rise to the Bitcoin and how it was presented on the Consolidated Statements of Financial Position. Specifically:

| ● | Non-cash consideration, i.e., Bitcoin, that is received in exchange for its computational power as part of the core of the Company’s operating activities and the sale of the associated Bitcoin that occurs within the Company’s normal operating cycle are reported among cash flows from operating activities. |

| ● | Bitcoin that the Company purchases and subsequently sells are reported among cash flows from investing activities since the generation of the Bitcoin did not arise from the Company’s operating activities (the Bitcoin was not received in exchange for its computational power) but rather from actions conducted expressly as an investment activity. |

1

For the year ending December 31, 2022, the Company presented the monetization of Bitcoin in both operating and investing sections of the Consolidated Statements of Cash Flows given that both of the categories described above were applicable.

IAS 7.16(b) refers to cash receipts from sales of property, plant and equipment, intangibles and other long-term assets, which all represent long-term assets. As described in the response to Comment 4 below, the Company considers Bitcoin to be a current asset due to its liquid nature and the presence of ready markets to exchange Bitcoin for cash, as well as the Company’s express intention to use the Bitcoin to meet the Company’s operating cash requirements as the need arises. Accordingly, given the character and intended application of the Bitcoin, the Company believes that presenting Bitcoin as a current asset is a more appropriate characterization of its actual application. For these reasons, the Company does not believe its treatment of Bitcoin should be within the scope of IAS 7.16(b) except where the Company purchases Bitcoin.

The Company has benchmarked its presentation against the presentation in the financial statements by its peers in their filings with the Commission and observed that its approach is consistently utilized by others within the industry and under International Financial Reporting Standards (“IFRS”).

As for the general time frame the Company holds its Bitcoin mined, the Company does not track, nor would it be practicable or useful for the Company to track, which of its Bitcoin are held and which of its Bitcoin are sold since they are a “fungible” asset that is accumulated in the same digital wallets. The Company does, however, maintain records concerning the Bitcoin held in treasury versus the daily production sold and clarifies for the Staff that:

| ● | The minimum time the Company held Bitcoin during the periods presented was a few hours, since the Company is primarily selling on a daily basis the majority of its daily production. |

| ● | The maximum time the Company held Bitcoin during the periods presented was approximately 12 months, as the Company began accumulating Bitcoin in early 2021 and commenced selling it in early 2022 as cash needs arose. However, from early 2022 to the current date, the Company typically sells the majority of its Bitcoin mined on a daily basis primarily in order to fund working capital needs. |

| ● | The average time the Company held Bitcoin during the years ended December 31, 2021 and 2022 was approximately 11 months and 1 month, respectively. The average time Bitcoin was held, as presented here, was based on the turnover calculation described in the response to Comment 4. |

2

| 2. | Please provide us your analysis supporting your revenue recognition policy for your mining pool participation activities. In your response, where appropriate, reference for us the authoritative literature you relied upon to support your accounting: |

| ● | Provide us a representative sample contract and cross reference your analysis to the specific provisions of that contract. |

| ● | Tell us how the amount of consideration is determined under the contracts and the payment methods. |

| ● | Tell us why you measure the non-cash consideration you receive for your mining activities based on the price quoted on the day you receive the digital assets. |

| ● | Relate your response to your disclosure that revenues from cryptocurrency mining are recognized when the computing power is provided to the mining pool. |

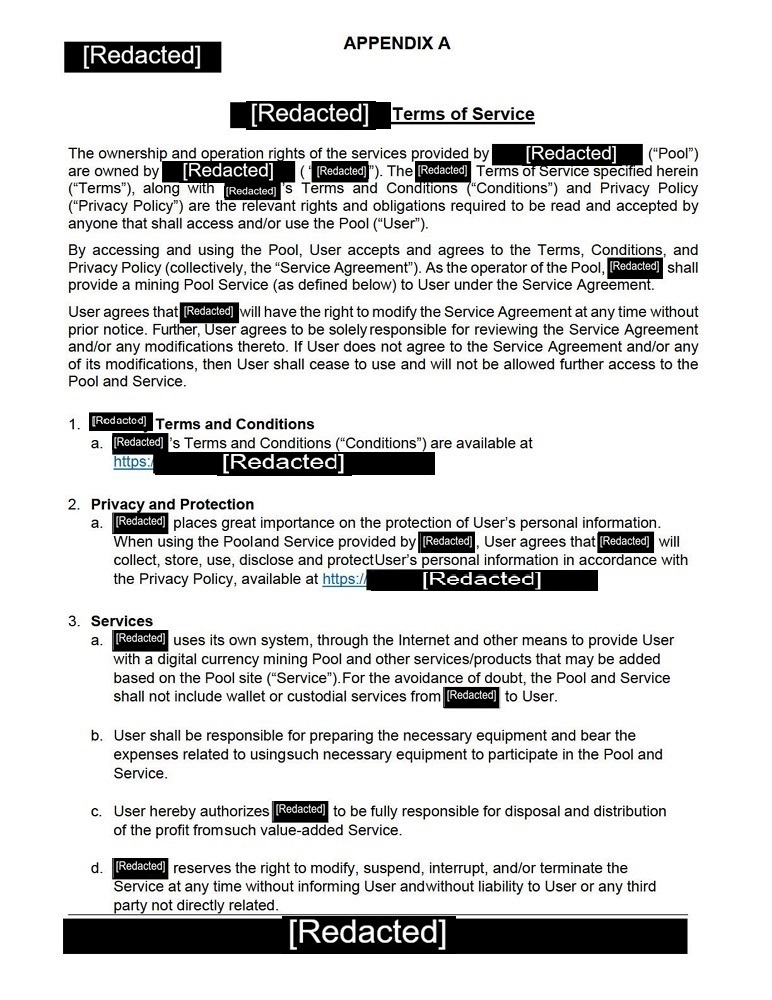

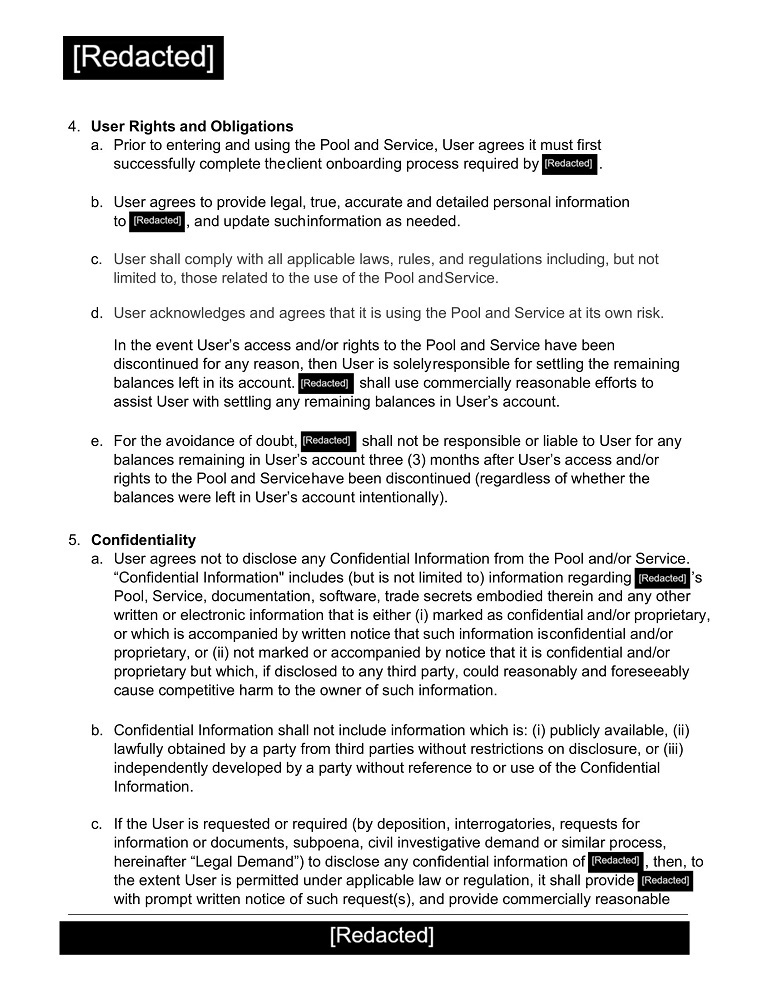

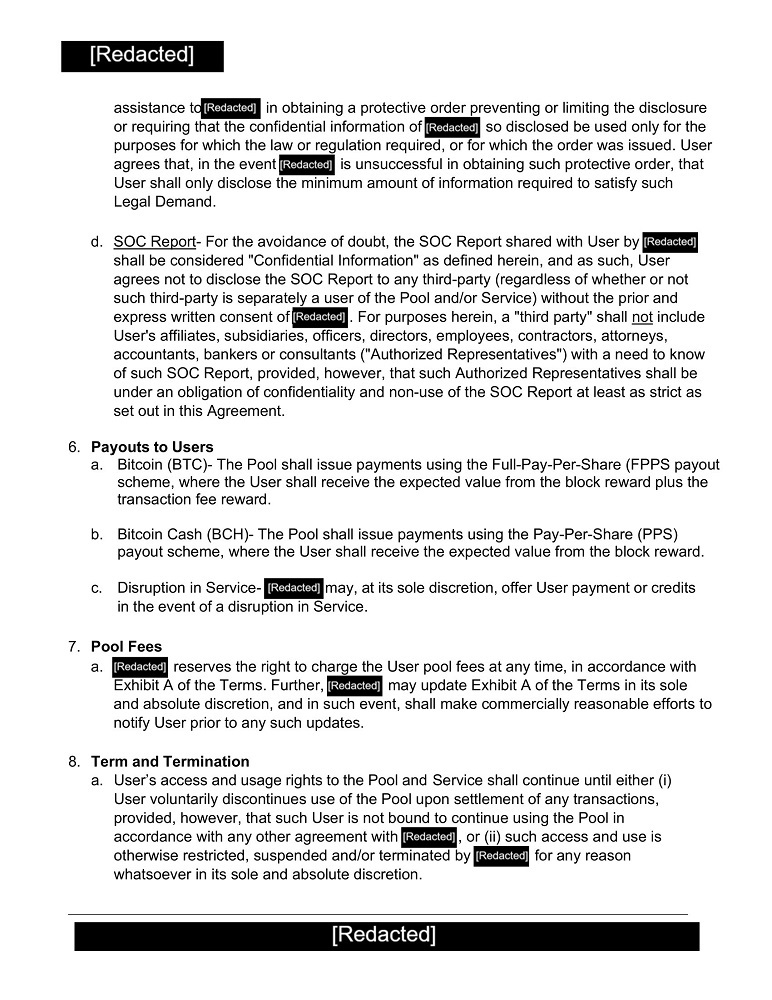

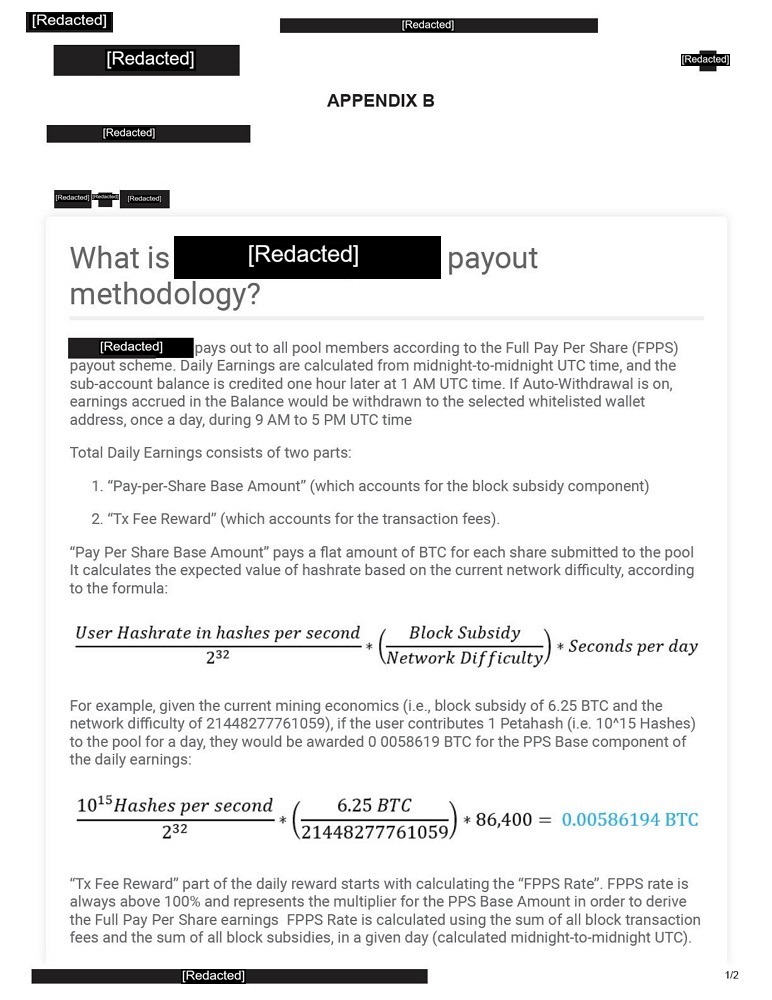

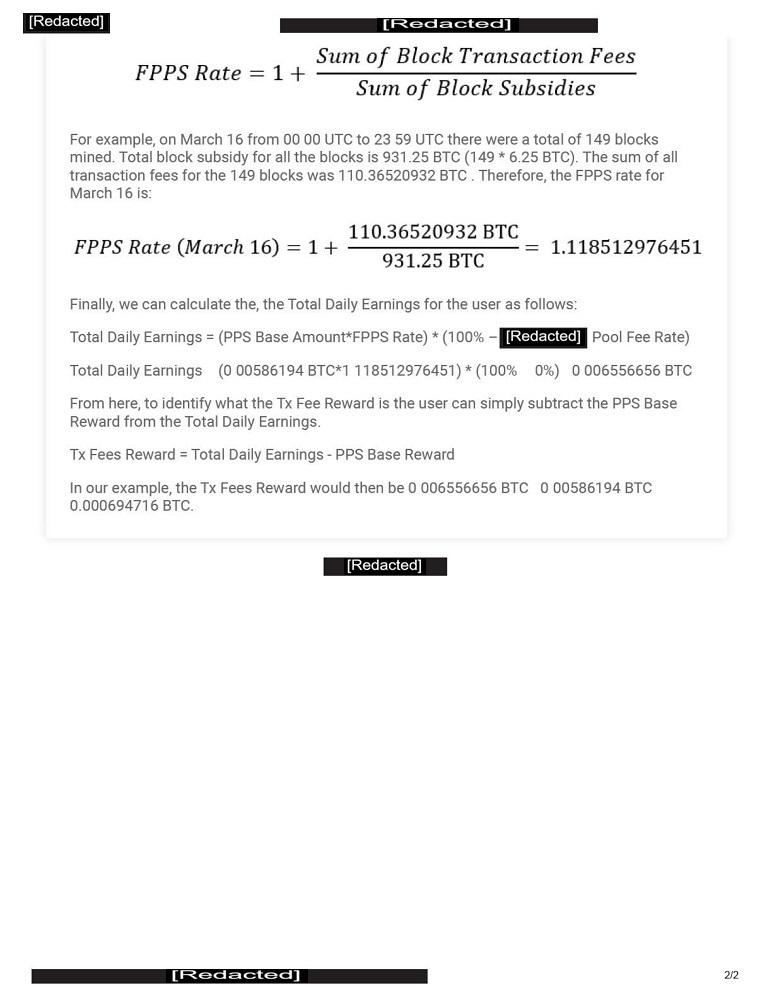

Response: In response to the Staff’s comment and in support of the Company’s revenue recognition policy for its mining pool participation activities, which are summarized below, the Company has included as Appendix A hereto a copy of its sole mining pool service agreement (the “service agreement”), which the Company has redacted because the redacted information is both (i) not material and (ii) would be competitively harmful if publicly disclosed. The Company agrees to furnish supplementally an unredacted copy of the service agreement to the Commission upon its request. Under the service agreement, the consideration paid to the Company is determined according to the Full-Pay-Per-Share “FPPS” payout scheme (as explained in more detail in Appendix B hereto). The Bitcoin earnings are derived from the Company’s allocated proportional hashrate contribution to the mining pool, assessed over a 24-hour period, and disbursed daily. The daily Bitcoin earnings consist of two distinct components:

| a) | The Company’s share of the expected block rewards; and |

| b) | The Company’s share of the expected transaction fees. |

Bitfarms’ agreement with the mining pool does not fit into the four exceptions of IFRS 15.5 which would require the Company to account for its earnings from its mining pool participation activities outside of IFRS 15; therefore, the contract is accounted for within the scope of IFRS 15, which requires the Company to:

| 1) | Identify the contract. |

| a. | This contract is identified as the mining pool service agreement (Appendix A), which has commercial substance. |

| b. | The Company transfers its hashrate and receives Bitcoin based on the FPPS payout scheme (Appendix B). |

| 2) | Identify the performance obligations. |

| a. | The Company provides the mining pool with computing power (i.e., hashrate) for non-cash consideration (i.e., Bitcoin). |

| 3) | Satisfy the performance obligations. |

| a. | The Company’s hashrate is transferred to the mining pool over a 24-hour period, which is used to find the block in order to receive the block reward and transaction fees. |

| 4) | Determine the transaction price. |

| a. | The Company measures the Bitcoin earned and received from mining activities based on the price quoted on the day the Bitcoin are received as that measurement time is a few hours after the Company completes its performance obligation of providing its hashrate for 24 hours. The mining pool disburses to the Company the Bitcoin earned on a daily basis. |

3

| 3. | In future filings, please revise to disclose the following: |

| ● | The time frame of when the revenue is deposited into your wallet. |

| ● | Whether the digital assets are received in whole or fractions. |

Response: The Company acknowledges the Staff’s comment and will include the requested disclosure in its future annual reports and any other future filings with the Commission where a detailed description of its accounting principles is included. In terms of the time frame of when the revenue is deposited into the wallet, this occurs on a daily basis, and the Bitcoin earned is received in full, but can be distributed in fractions of Bitcoin. The Company is currently in the process of drafting its proposed disclosure, which has not yet been finalized at the date of this response letter.

| 4. | You classify your digital assets and pledged digital assets as current assets because management determined that the digital assets have markets with sufficient liquidity to allow conversion within your normal operating cycle. Please tell us how your classification of digital assets as current assets considered IAS 1, including paragraphs 66 - 68. In your response, at a minimum, address each of the following: |

| ● | For digital assets held at December 31, 2021 and 2022, tell us the average length of time the assets have been held and how frequently the assets turn over, explaining how you calculated this turnover. |

| ● | Tell us your consideration for carrying a portion of your holdings that are not expected to be sold for cash as long-term. |

Response: The Company believes its Bitcoin adheres to the criteria to be classified as current assets as per paragraph 66 of IAS 1, which states that an entity shall classify an asset as current when:

| ● | it expects to realise the asset, or intends to sell or consume it, in its normal operating cycle; |

| o | The Company sells its computing power, gets rewarded in Bitcoin and sells its Bitcoin to cover costs and expenses during its normal operating cycle. The Bitcoin are sold when needed for working capital purposes and, accordingly, should be classified as short-term. |

| ● | it holds the asset primarily for the purpose of trading; |

| o | The Company considers its Bitcoin to be a liquid asset, as it can be readily converted to cash as needed. |

| ● | it expects to realise the asset within twelve months after the reporting period; or |

| o | The Company’s December 31, 2022 year-end balance and turnover demonstrated that the Company expected to realize the asset within the next 12 months as a source of funds for operations. |

| ● | the asset is cash or a cash equivalent (as defined in IAS 7) unless the asset is restricted from being exchanged or used to settle a liability for at least twelve months after the reporting period. |

| o | Bitcoin is not considered cash or a cash equivalent as defined in IAS 7 due to its price volatility. |

The majority of the Company’s mined Bitcoin are sold within an operating cycle to cover its costs and expenses, which is supported by the turnover calculation below. The remaining Bitcoin are held within the Company’s treasury for the purpose of trading and used when needed.

4

For Bitcoin held at December 31, 2021 and 2022, the average length of time the assets have been held was approximately 11 months and 1 month, respectively. The turnover during the fiscal years ended December 31, 2021 and 2022 was approximately 1.1 and 15.2, respectively. To calculate the turnover, the Company added all the Bitcoin mined and purchased during the year and divided the summation by the balance of Bitcoin at the end of the year. The average length of time the assets were held was calculated by dividing 365 days by the turnover and then converting it from days to months.

| 5. | Regarding the determination of the fair value of your digital assets using the price quoted on Coinmarketcap, please respond to the following: |

| ● | Tell us the market in which you normally enter into transactions to sell your digital assets. |

| ● | Tell how you identify your principal market, explaining the process you undertook to evaluate various exchanges on which you trade and how this process and ultimate conclusion conforms to the guidance in IFRS 13. |

Response: The Company currently sells its Bitcoin through Coinbase and another corporate third-party in Canada that has a platform connected to the main cryptocurrency exchanges in the world with the objective of selling its Bitcoin at the “best” price across these multiple markets. The price across most markets is within a relatively tight range since the Bitcoin market is liquid. The Company mines and receives Bitcoin on a daily basis and uses the Bitcoin price from Coinmarketcap to determine the fair value. On a monthly basis, the Company compares the prices obtained from Coinmarketcap with the average daily price from Coinbase. The pricing difference at closing, if any, has not been material historically.

The Company uses Coinmaketcap because it is widely recognized as an established, trusted source for reliable pricing, and its pricing is similar to the pricing of Coinbase and other markets.

Further, Coinmarketcap has a direct connector through an application programming interface with the Company’s accounting system, which is a practical and efficient solution, allowing the information to be easily available and strengthening the Company’s internal controls.

| 6. | In future filings, please reconsider the appropriateness of your statements in the filing that there is no definitive guidance under IFRS for the accounting for digital assets recognized as revenue or held. We observe that for your company IFRS is the source of authoritative guidance and that there is guidance whose scope applies to your transactions. |

Response: The Company acknowledges the Staff’s comment and will include the requested disclosure in its annual reports and any other future filings with the Commission where a detailed description of its significant accounting judgements and estimates is included. The revised disclosure will explain that, although there is no specific guidance for cryptocurrencies under IFRS, judgement is still required due to the particular characteristics of mining and holding Bitcoin. The Company applies judgement to account for the revenue recognition from Bitcoin mining and subsequent remeasurement of Bitcoin held under IAS 38, Intangible Assets (“IAS 38”). In the event that new guidance is issued by the International Account Standards Board, the Company would as appropriate change its accounting policies, which could have a material effect on the Company’s financial statements. The Company is currently in the process of drafting its proposed disclosures, which has not yet been finalized at the date of this response letter.

5

| 7. | Please respond to the following: |

| ● | Give us your rollforward of digital assets with the removal of the BTC exchanged for cash (i.e., proceeds from sales of BTC) and realized loss on disposition of digital assets and replace them with the carrying value of the cryptocurrencies sold for cash. |

| ● | In future filings, similarly revise the rollforward in your disclosure to reflect the carrying value of digital assets sold and include sufficient supplementary disclosure below the reconciliation to relate the carrying value of cryptocurrencies sold to the realized gains or losses on digital assets sold on your statements of operations and the amounts within your statements of cash flows. |

| ● | Tell us why the digital assets issued for services are not reflected in the significant non-cash transactions shown on page 61. |

Response: In response to the Staff’s comment, the Company has provided below the rollforward of its Bitcoin holdings for the years ended December 31, 2022 and December 31, 2021 with the requested changes:

| Année terminée le 31 décembre, | ||||||||||||||||

| 2022 | 2021 | |||||||||||||||

| Quantité | Valeur | Quantité | Valeur | |||||||||||||

| Solde des actifs numériques, y compris les actifs numériques donnés en garantie, au mois de janvier 1, | 3,301 | 152,856 | — | — | ||||||||||||

| BTC mined | 5,167 | 138,985 | 3,453 | 164,393 | ||||||||||||

| BTC achetés | 1,000 | 43,237 | — | — | ||||||||||||

| Carrying value of BTC exchanged for cash and services and long-term debt repayment | (9,063 | ) | (330,539 | ) | (152 | ) | (6,676 | ) | ||||||||

| Variation du gain (perte) non réalisé(e) sur la réévaluation des actifs numériques | — | 2,166 | — | (4,861 | ) | |||||||||||

| Solde des actifs numériques au mois de décembre 31, | 405 | 6,705 | 3,301 | 152,856 | ||||||||||||

| Less digital assets pledged as collateral as of December 31, | (125 | ) | (2,070 | ) | (1,875 | ) | (86,825 | ) | ||||||||

| Solde des actifs numériques à l'exclusion des actifs numériques donnés en garantie au mois de décembre 31, | 280 | 4,635 | 1,426 | 66,031 | ||||||||||||

The Company believes that presentation of Bitcoin exchanged for cash and services and the realized loss on disposition of Bitcoin on a disaggregated basis provides the users of the Company’s financial statements with a more comprehensive rollforward of Bitcoin. The rows included in the rollforward of the Company’s Bitcoin holdings for the years ended December 31, 2022 and 2021 provide information to the users of the financial statements that ties directly with line items in the statement of operations and statement of cash flows and assist the users in understanding the impact throughout the financial statements. In light of the foregoing, the Company respectfully requests that the Staff not object to the Company’s disclosure of the rollforward in its future filings on a basis consistent with its historical practices.

6

The Bitcoin exchanged for services were not reflected in the significant non-cash transactions as management determined such amounts to be not material. In addition, the contracts that gave rise to the services being exchanged for Bitcoin were terminated at the end of 2022. The Company currently exchanges Bitcoin for services occasionally, in the event that aggregate services exchanged for Bitcoin are determined by management to be material, the amounts will be disclosed separately.

| 8. | You disclose that the disposition of the marketable securities in exchange for Argentine Pesos gave rise to a gain as the amount received in ARS exceeds the amount of ARS you would have received from a direct foreign currency exchange. Please tell us in more detail about the nature of the gain on disposition of marketable securities and how you measured the amount of the gain. |

Response: Beginning in the second half of 2019, the Argentine government instituted certain foreign currency exchange (“FX”) controls that could restrict the Company’s wholly-owned Argentinian subsidiary’s (Backbone Hosting Solutions SAU) access to foreign currency, including the U.S. dollar, for making payments abroad or transferring funds to the Company without prior authorization from the Argentine Central Bank. Those regulations have continued to evolve and may become more stringent depending on the Argentine government´s perception of availability of sufficient national foreign currency reserves, including the U.S. dollar.

In response to these exchange controls, markets in Argentina implemented a multi-FX rate structure to encourage trade activity. Utilizing these different FX rates under a trading mechanism referred to as a “Blue Chip Swap”, commercial and financial enterprises are afforded a favorable exchange rate when they sell U.S. dollars and exchange them for Argentine pesos. This implicit Blue Chip exchange rate differs from the official exchange rate.

The Company has utilized the Blue Chip Swap mechanism to convert its U.S. dollar holdings into Argentina pesos to fund its Argentina expansion through the acquisition of marketable securities and in-kind contribution of those marketable securities to Backbone Hosting Solutions SAU. The subsequent disposition of those marketable securities in exchange for Argentine Pesos using the Blue Chip Swap mechanism gave rise to a gain as the equivalent amount received in Argentine Pesos exceeded the amount of Argentine Pesos the Company would have received at the official exchange rate. The Company’s Argentinian subsidiary’s functional currency is U.S. dollars. Argentina peso-denominated monetary assets and liabilities are remeasured at each balance sheet date to the official currency exchange rate then in effect, which represents the exchange rate available for external commerce (import payments and export collections) and financial payments, with currency remeasurement and other transactions gains and losses recognized in earnings. Any gain on disposition of marketable securities therefore goes though the statement of profit or loss rather than the statement of other comprehensive income. As the Company converts the foreign currency translation using the official exchange rate and not the favorable exchange rate from the Blue Chip Swap mechanism, the difference in translation at the time of the transaction between the implicit Blue Chip exchange rate that the Company receives for the funds sent and the official rate that the Company applies for reporting purposes represents the amount of the gain, which is recorded in net financial income.

* * * * *

7

The Company plans to incorporate the new disclosures noted throughout this response letter beginning with its annual report for the year ending December 31, 2023.

In connection with responding to the Staff’s comments, the Company acknowledges that it is responsible for the accuracy and adequacy of the disclosures in its filings, notwithstanding any review, comments, action or absence of action by the Staff.

We believe that the responses above fully address the comments contained in your Letter. If you have any questions regarding the 2022 40-F or the above responses, please contact the undersigned at 617-504-1243 or jlucas@bitfarms.com or Mark D. Wood of our U.S. counsel Katten Muchin Rosenman LLP at 312-902-5493 or mark.wood@katten.com.

Cordialement,

| /s/ Jeffrey Lucas | |

| Jeffrey Lucas | |

| Directeur financier |

8